Online Shopping UK Revenue Growth 2017

Clients often ask me how their online revenue performance compares to industry growth and competitor eCommerce sites. Sound familiar? I’m sure many of you have asked (or been asked) the same question.

Comparing online revenue performance is difficult because there are so many variables at play and unless you have analytical access to a variety of websites eCommerce reporting/statistics, it can be difficult to answer this question. Often it comes from one of two places:

1. We want reassurance - when we experience a decline in performance, we like to feel a sense of camaraderie with our competitors; ‘is this happening to you?’ (hoping the answer is ‘yes’) which usually satisfies us, indicating the decline is seasonal or there’s external factors at play. However, repetitive declines often lead to cost-cutting (understandably) and I often see Marketing is the first expense to be lobbed (sigh!).

Or

2. We’re competitive and self-critical - we’ve seen an increase in online sales and we want to understand if the percentage increase is good enough! Not only that… we usually want to prove what drove this positive performance (I’m not knocking that… we don’t want to get complacent just because things are good right now). The questions I find which follow are: How do we compare? How do we know it’s not just a natural rate of inflation? And then again, the marketing comes into question… usually to justify if it contributed in any way to the growth seen (big sigh!).

In 2016 UK online sales were reported to have increased by 21.3% year on year, with 2017 set to see highs of a 30% increase.

So, I thought I would do a little comparing of our ThoughtShift eCommerce clients within the retail industry, to 2017 performance reported in the UK thus far instigated from wanting a little ‘reassurance’ (for myself and my clients) plus, because I’m a marketer… I’m immensely self-critical.

2017’s UK eCommerce Predictions and Progress

It’s reported that the UK is the second highest online purchasing country in Europe, so it wasn’t surprising to read that 87% of consumers in the UK had made at least one online purchase last year. With online sales reported to have increased by 21.3% in 2016 year on year and 2017 set to see highs of a 30% increase, the talks of what impact leaving the EU would have on both suppliers and consumers has placed some doubt across the consumer behaviour we’re likely to witness over the next year or so. Regardless of whether you have bricks and mortar stores in addition to eCommerce, the world of digital online shopping is no longer a luxury to have but a necessity especially with 70% of millennials reported to think they can gain better access to information online vs. in store. I’ve been keeping an eye on reports of UK’s eCommerce sales performance this year to date:

Q1

- January reported a 16% year on year increase in online revenue, partly attributed to an increase in average order value (£85 vs. £79) with the gifts sector seeing the highest percentage increase (62%) and electronics suffering the biggest decline (-12%). However, 2017 also reported the smallest year on year growth since 2012.

- February reported online sales growth of 20.7%, accounting for 15.3% of total retail spending and up 3.3% on January breaking the trend of declining sales.

- March reported that UK consumers spent £1bn per week across March 2017 boasting a 19% increase vs. 2016, though in store sales saw a 3% decline. This contributed to 15.9% of retail sales across the UK vs. a 13.9% increase the previous year, with non-food online sales increasing 6.6% but we must consider the fact Easter was much later in 2017. Sectors such as fashion and textiles saw the biggest revenue growths vs. 2016 (28.1%).

Q2

- April reported an avg. 14% year on year increase in online sales, again attributed to a weekly spend of £1bn which was a 19% increase on 2016’s weekly spend.

- May saw a 4.3% increase in non-food online sales vs. 2016, which the British Retail Consortium described as ‘meagre’ which with a total 13% annual increase across all online sales, it’s fair to agree with May achieving the weakest annual percentage growth this year to date.

- Jun reported a slight increase in weekly online spend to £1.1bn, a 15.6% increase in the weekly avg. seen in 2016 however total online sales saw year on year growth of 10%, the slowest recorded since 2004 despite accounting for 22% of total sales across retail. This is thought to be by and large a result of the scorching UK weather we experienced which meant consumers were out and about, not necessarily shopping online (let’s not forget Amazon Prime day, but even that didn’t seem to be the digital revenue boost for the UK). The weather seemed to help retail (stores mainly) performance as a whole with a 5.7% increase reported (1.2% if you exclude store closures and openings).

With Q1 seeing an avg. annual growth of 18.6% and Q2 reporting a smaller avg. growth of 12.3%, I wanted to look at how our eCommerce clients were fending in comparison.

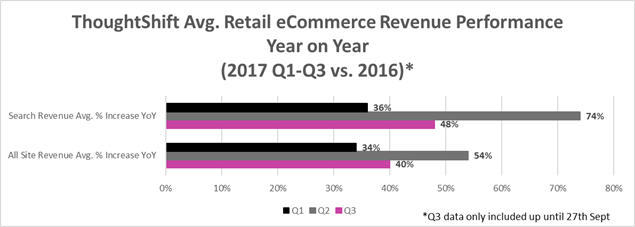

ThoughtShift eCommerce Clients Grew Search Revenue by 53% on Average Q1-Q3 2017

Okay… so given that the above doesn’t report on online revenue by traffic source it would be unfair of me to only analyse search performance.

ThoughtShift clients saw an average revenue increase from all site traffic of 43% year on year

I therefore collated All Site revenue performance per quarter (starting to report into Q3) and was very pleased with the results (if I do say so myself):

ThoughtShift eCommerce clients on avg. saw annual retail revenue growth of:

- 43% year on year from All Site traffic

- 53% year on year from Search traffic alone

Not too shabby in comparison to the UK online sales average.

Now, making an exception for the fact I haven’t broken this down by industry (for client confidentiality) which audience do you currently fall into? One who feels reassured or one who is now criticising their online performance?

Whichever category you fall into, I’d like to demonstrate why cutting off your digital marketing channels (particularly search) may not be the best approach to take:

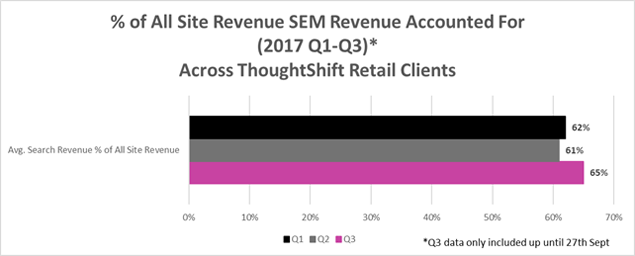

Search channels have accounted for on avg. 63% of All Site eCommerce revenue in 2017 to date across ThoughtShift clients. More than half, which without good search visibility, wouldn’t have been achieved and is a rather large chunk of revenue to cut off.

Another question I’m often asked is ‘what’s a good conversion rate for eCommerce?’ but I’ll let Helen catch you up on that. Hopefully looking at the UK’s sales performance is making you feel more comfortable with your own online sales performance. If not… maybe it’s worthwhile investing more in digital channels?

*Data exported from UK eCommerce clients only within retail.

For more eCommerce and online shopping statistics, join the ThoughtShift Guest List and get the latest blogs delivered to your inbox each month or ask us for a free eCommerce marketing analysis of your website.